When you walk into a professional workspace—whether it’s a law firm, a dental clinic, or a corporate headquarters—the artwork on the walls sets the tone. It creates a welcoming atmosphere for clients and an inspiring environment for employees. But did you know that investing in original art does more than just elevate your company’s aesthetic? It can also be a highly strategic, tax-deductible financial decision.

The Canadian government actively encourages businesses to support the local arts and culture sector by offering significant tax incentives. When a business purchases an original work by a Canadian artist, the Canada Revenue Agency (CRA) allows it to be claimed as an amortizable capital asset.

Here is everything you need to know about how your business can benefit financially from acquiring Canadian art.

Who Can Claim the Deduction?

These tax incentives are available to corporations and individuals who operate a business. As long as the purchase is made by the business and for the business, you can take advantage of these rules.

The Criteria: What Qualifies as a Tax-Deductible Art Purchase?

Not every poster or print will qualify for a tax write-off. To satisfy CRA guidelines, your art acquisition must meet four specific criteria:

-

It Must Be by a Canadian Artist: The artwork must have been created by an artist who was a Canadian citizen or a permanent resident at the time the piece was made.

-

It Must Be Original: The piece must be an original work of visual art. This includes paintings, sculptures, drawings, and limited-edition prints. Mass-produced reproductions do not qualify.

-

It Must Meet the Value Threshold: To be classified as a depreciable asset rather than a simple one-time expense, the artwork must generally cost more than $200.

-

It Must Serve a Business Purpose: The artwork must be acquired with the intention of earning business income. Practically speaking, this means the art must be displayed in a commercial environment where it can be seen by clients, customers, or employees. Eligible spaces include reception areas, boardrooms, lobbies, hallways, and client-facing offices. (Note: Art hidden away in a private home for personal enjoyment does not qualify).

How the Tax Deduction Works (CCA Class 8)

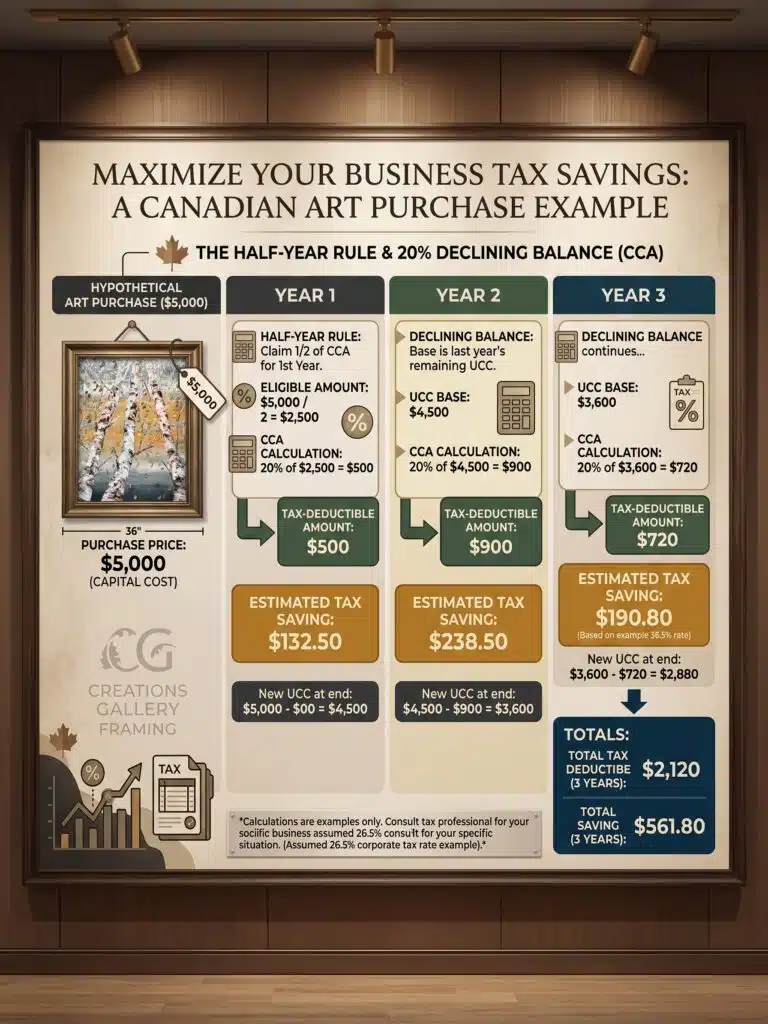

When your business purchases a qualifying piece of Canadian art, the CRA considers it a depreciable asset. This means you do not write off the entire cost in a single year; instead, you claim the cost over several years through the Capital Cost Allowance (CCA) system.

Artwork is classified as a Class 8 asset. This allows your business to deduct 20% of the artwork’s declining value from your taxable income each year.

The Half-Year Rule: In the very first year you purchase the art, the CRA’s "half-year rule" applies. This means you can only claim 50% of the standard deduction rate in year one (effectively a 10% deduction). In year two and beyond, you can claim the full 20% on the remaining balance.

Recovering Sales Tax (GST/HST/QST)

If your business is registered to collect GST, HST, or QST, you can recover the sales taxes paid on your art purchase. These amounts can be claimed as Input Tax Credits (ITCs) on your regular tax returns, effectively lowering your initial out-of-pocket costs.

What Happens If You Sell the Artwork Later?

Art is a unique corporate asset because, unlike office furniture or computers, it has the potential to appreciate in value over time. If your business decides to sell the artwork down the road, there are two potential tax scenarios:

-

Selling for a Profit: If the piece appreciates and you sell it for more than your original purchase price, the amount you previously claimed as a CCA deduction will be subject to "recapture" (counted as business income). Any actual profit above the original purchase price will be taxed as a capital gain.

-

Selling at a Loss: If you sell the artwork for less than its remaining undepreciated cost, you can claim the difference as a terminal loss, which further reduces your taxable business income.

Invest in Art, Invest in Your Business

Transforming your office space doesn't have to be a sunk cost. By intentionally selecting original works by Canadian artists, your business is directly contributing to the nation's vibrant cultural economy while retaining more capital in your pocket.

Browse our curated collection of Corporate-Ready Canadian Art, or link directly to the profiles of our featured Canadian artists.

Disclaimer: We are art professionals, not accountants! Tax laws can be complex and specific to your individual business structure. We highly recommend consulting with your Chartered Professional Accountant (CPA) to ensure these guidelines apply correctly to your business before filing.

🏛️ Verify the Facts: Official Government of Canada Sources

Want to verify these rules directly with the Canada Revenue Agency? We encourage you and your accountant to review the official Government of Canada (Canada.ca) guidelines below:

-

Claiming Capital Cost Allowance (CCA): An overview of how businesses can deduct the cost of depreciable property over time.

-

CCA Classes (Class 8): Details the 20% depreciation rate for Class 8 assets, which includes artwork purchased for business use.

-

Terminal Loss and Recapture: Explains what happens when you sell a depreciable asset for more or less than its remaining value.

-

Input Tax Credits (ITCs): Information on claiming back GST/HST paid on eligible business purchases.